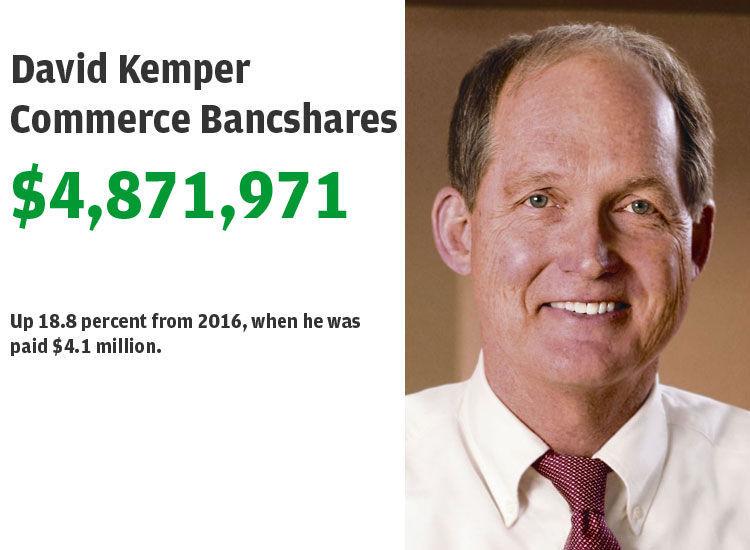

Very few businesses of any size are led by a sixth generation of the same family. The number of sizable, highly regulated public companies is infinitesimal.

At Commerce Bancshares, though, John Kemper took over Aug. 1 as chief executive of the nationŌĆÖs 45th-largest bank. He succeeds his father, David, and a long line of family members starting with his great-great-great grandfather, William S. Woods, who bought a small Kansas City bank in 1881.

In an interview at his Clayton office, Kemper sounded humble about his predecessorsŌĆÖ legacy, but confident that he can live up to their standards. The familyŌĆÖs ŌĆ£secret sauce,ŌĆØ he said, boils down to a solid business model and continuity of vision.

People are also reading…

ŌĆ£The organizationŌĆÖs transition from David Kemper to John Kemper is going to be one of degrees of difference, not wholesale change,ŌĆØ the 40-year-old CEO said. ŌĆ£WeŌĆÖre both very results-focused leaders.ŌĆØ

Results have earned the Kemper family, which owns less than 5 percent of CommerceŌĆÖs stock, the right to keep running the company. Commerce has survived financial panics from 1893, when 500 other banks failed, to 2008, when it was one of the largest banks that didnŌĆÖt accept bailout money.

Shareholder returns amounted to nearly 15 percent a year during David KemperŌĆÖs 32 years as CEO, compared with 10 percent for the broad stock market.

Commerce excels at a no-surprises style of banking with high credit standards, plenty of capital and gradual but steady growth.

ŌĆ£If you want to sum it up with a couple of easy words, IŌĆÖd say strength, security and vision,ŌĆØ says banking analyst Joseph Stieven, who runs Stieven Capital Advisors. ŌĆ£They have always been one of the soundest banks in the U.S.ŌĆØ

Commerce calls itself a ŌĆ£super-community bank,ŌĆØ with a branch network stretching from Denver to central Illinois and a few specialty businesses, such as corporate payments, that compete nationwide.

In an industry where giant banks are under extreme scrutiny from regulators and little banks struggle to keep up with technology, Kemper thinks middle-sized is a good thing to be.

ŌĆ£WeŌĆÖve found kind of a sweet spot,ŌĆØ he says. ŌĆ£The small banks, a lot of them are sub-scale, and on the big side thereŌĆÖs a different set of challenges. They have incredible R&D budgets, but have a hard time getting their ducks in a row when it comes to delivering services.ŌĆØ

Kansas City and ║³└Ļ╩ėŲĄ, which Commerce considers dual headquarters, are by far the bankŌĆÖs biggest markets, but much of its loan growth lately has come from places such as Denver, Dallas and Cincinnati. Commerce has only commercial lending offices in the latter two cities.

That model involves hiring lenders, payment experts and other corporate specialists in each market. ItŌĆÖs a faster path to profitability than buying or building full-service branches, Kemper says.

The new CEO has been a ║³└Ļ╩ėŲĄan since age 7, when his father moved here to run CommerceŌĆÖs ║³└Ļ╩ėŲĄ operations. Following his fatherŌĆÖs example, he has become involved with several local civic institutions.

He spent three years as board chairman at┬Ā, which runs five charter schools, and says education is a personal passion. ŌĆ£They are delivering results in a part of our community that desperately needs help,ŌĆØ Kemper says. ŌĆ£I see education as a platform issue for ║³└Ļ╩ėŲĄ that needs our full attention.ŌĆØ

ItŌĆÖs also a business issue: The bank and its customers need future workers, and Commerce canŌĆÖt thrive if ║³└Ļ╩ėŲĄ doesnŌĆÖt.

ŌĆ£We recognize that our fortunes are going to ebb and flow with those of the local economy,ŌĆØ Kemper said.

Meet the 30 top-paid CEOs in ║³└Ļ╩ėŲĄ, 2017 pay

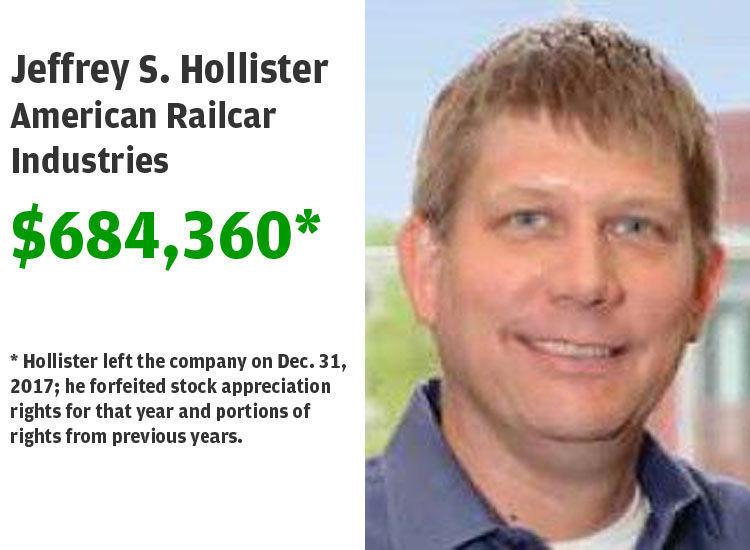

* Jeffrey S. Hollister, American Railcar Industries

Hollister left the company on Dec. 31, .╠²

30. Timothy D. Boyd, Peak Resorts

In January, .

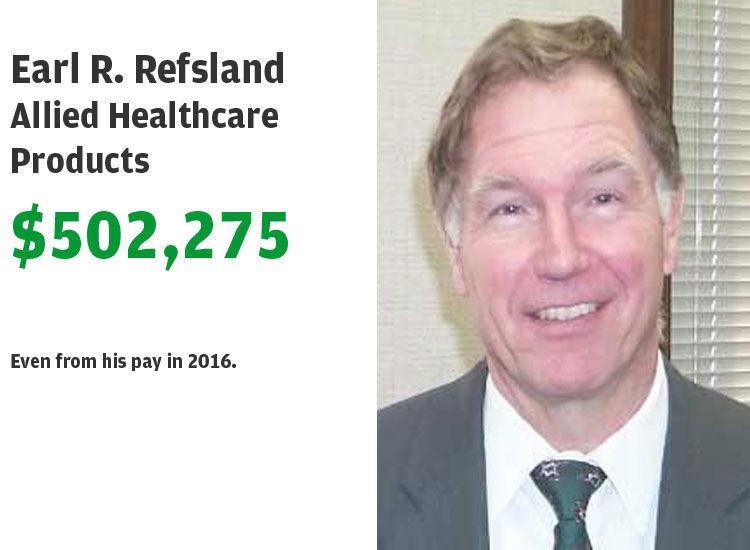

29. Earl R. Refsland, Allied Healthcare Products

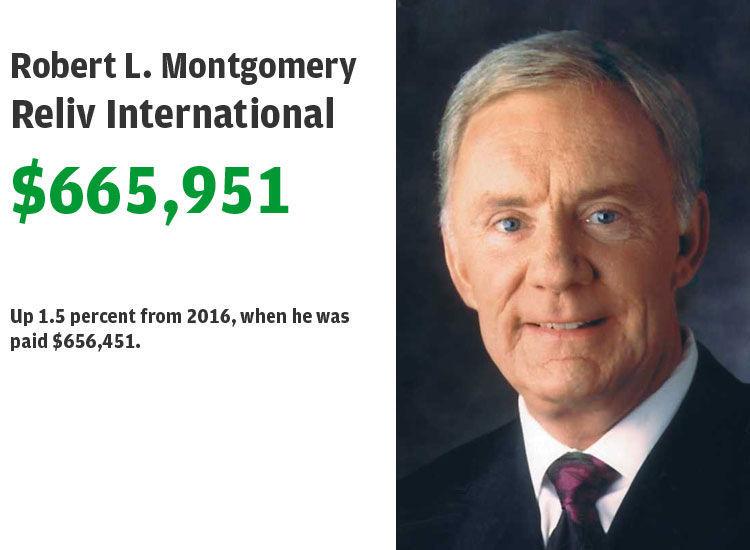

28. Robert L. Montgomery, Reliv International

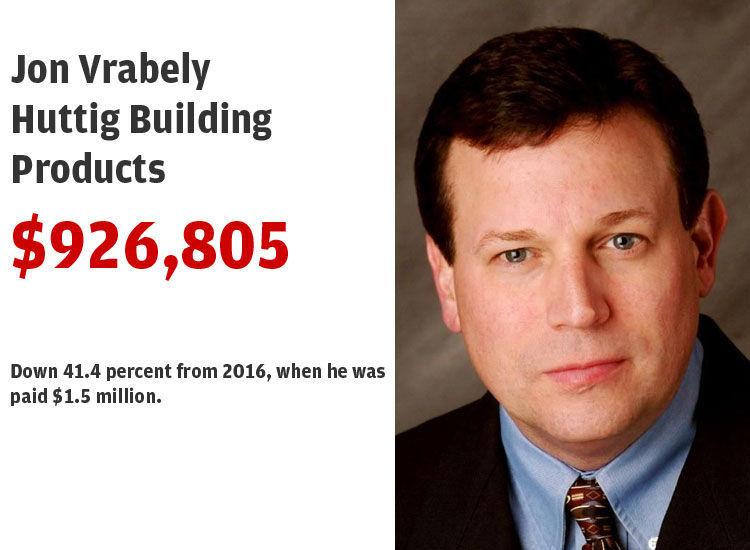

27. Jon P Vrabely, Huttig Building Products

; CEO earned 20 times as much as median Huttig employee. The company says its 1,300 full- and part-time workers earn a median of $47,091.

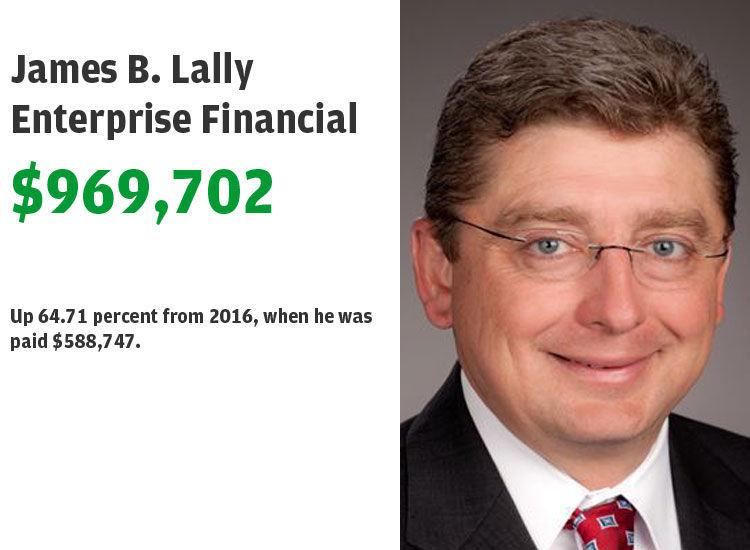

26. James B. Lally, Enterprise Financial

.╠²Enterprise calculates that the CEO made 16 times as much as its median employee, who earned $60,000.╠²

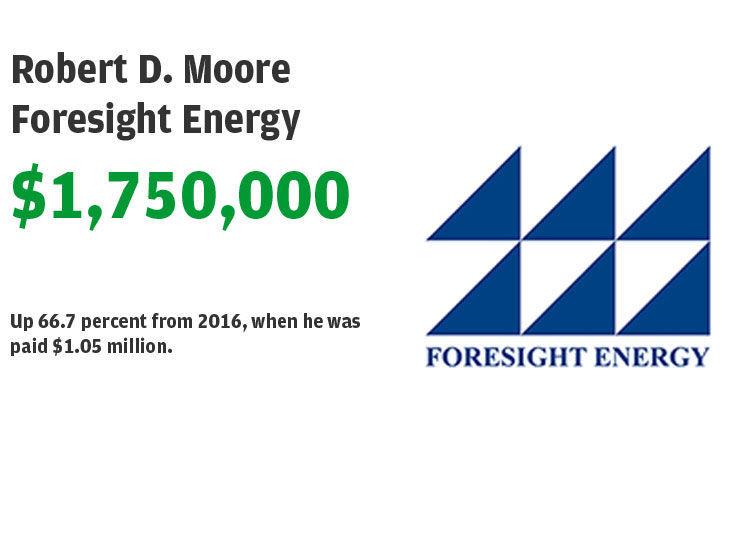

25. Robert D. Moore, Foresight Energy

From March:┬Ā

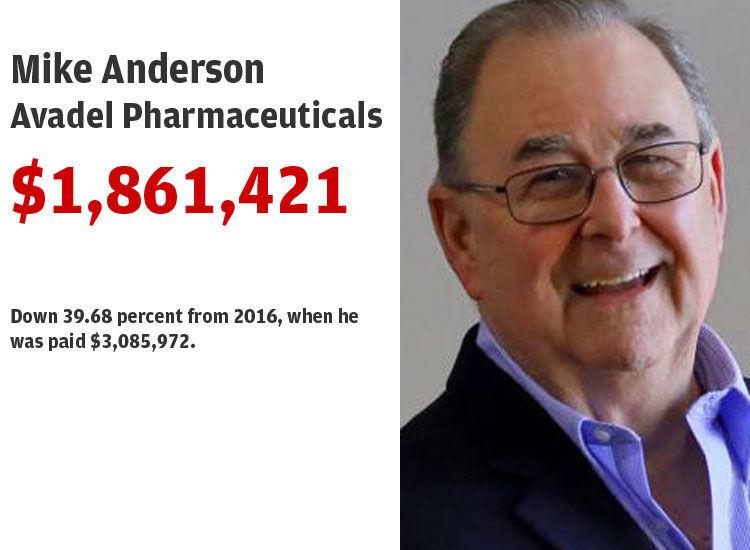

24. Mike Anderson, Avadel Pharmaceuticals

.

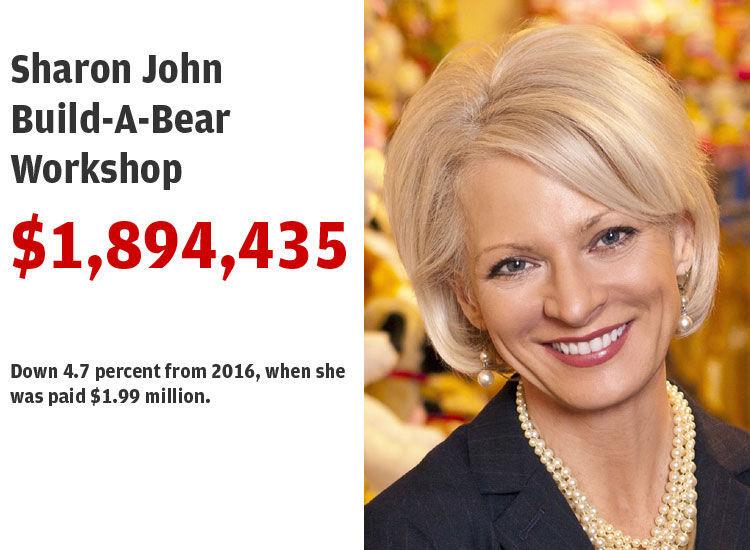

23. Sharon John, Build-A-Bear Workshop

;╠²John earned 306 times as much last year as the median Build-A-Bear employee. Median pay was $6,198 for the Overland-based company's 4,455 U.S. and British workers.╠²

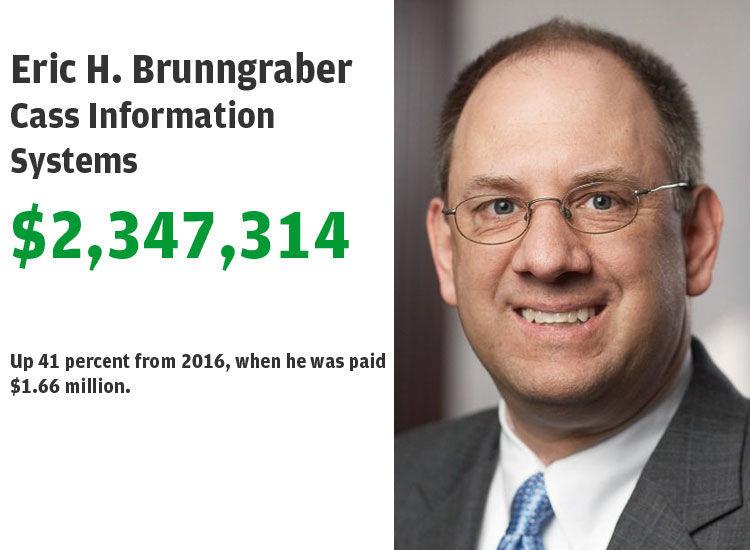

22. Eric H. Brunngraber, Cass Information Systems

21. Charles R. Gordon, Aegion

;╠²Gordon made 36 times as much as the median employee's compensation of $73,848. The Chesterfield-based pipe-repair company employs 6,242 people worldwide.

20. V.L. Richey Jr., Esco Technologies

19. Suzanne Sitherwood, Spire

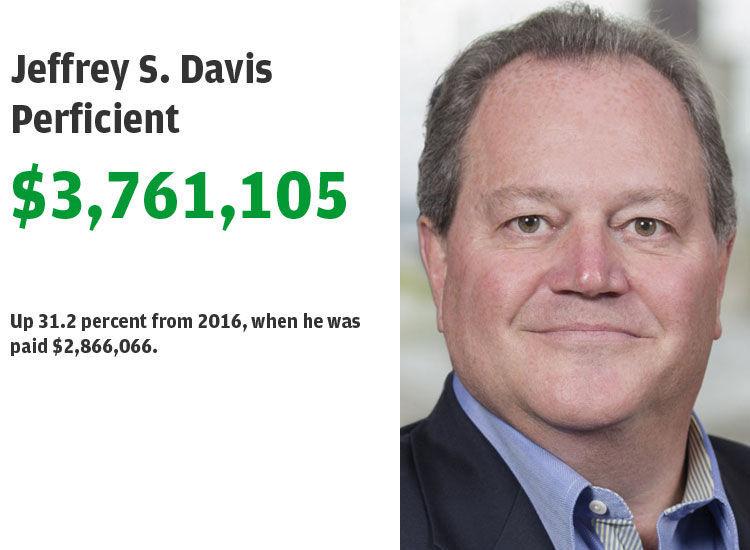

18. Jeffrey S. Davis, Perficient

. Its 2,078 workers in the United States, China and India earned a median $96,193.

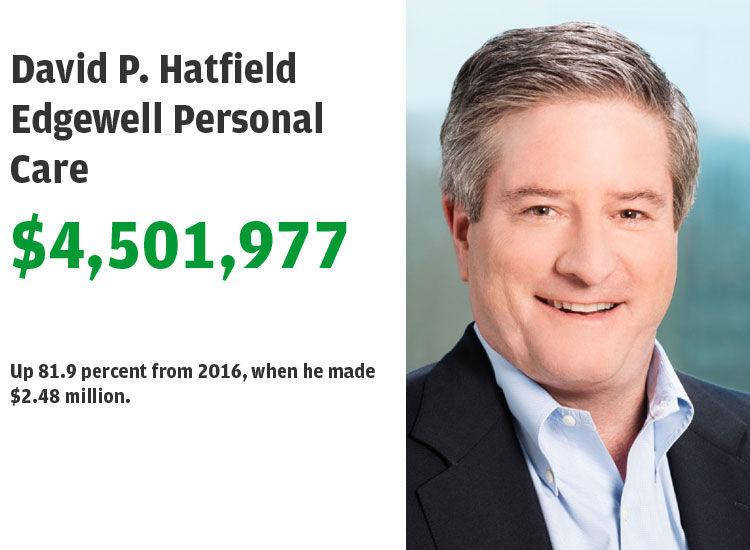

17. David P. Hatfield, Edgewell Personal Care

16. David Kemper, Commerce Bancshares

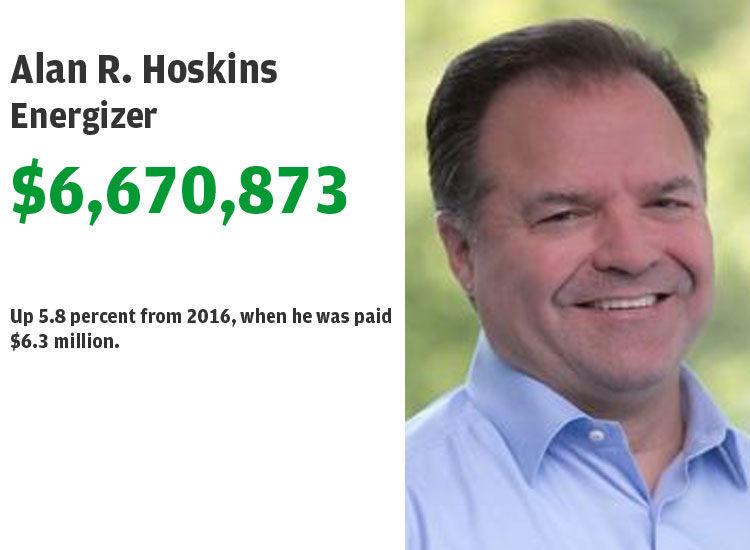

15. Alan R. Hoskins, Energizer

From January:

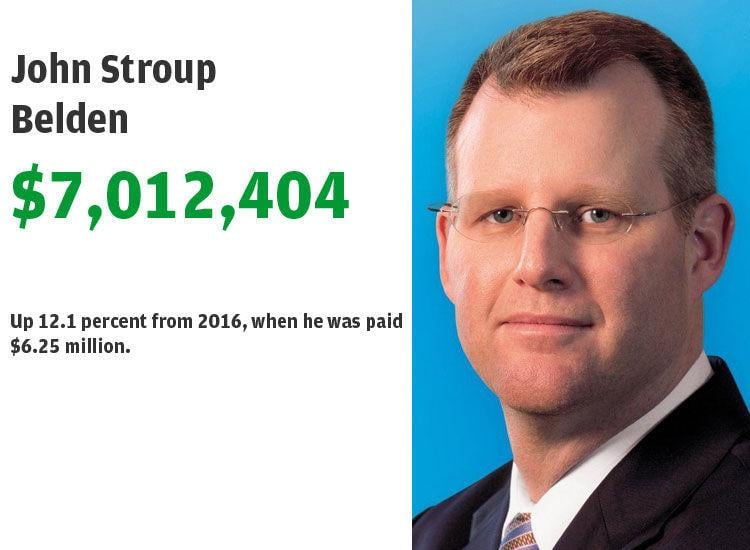

14. John Stroup, Belden

;╠²the CEO earned 133.6 times as much as the median Belden worker, who made $52,487 last year.

13. Anna Manning, Reinsurance Group

;╠²Manning's pay is 66 times as much as the median employee earned last year. Median pay for the company's 2,741 employees was $107,171.

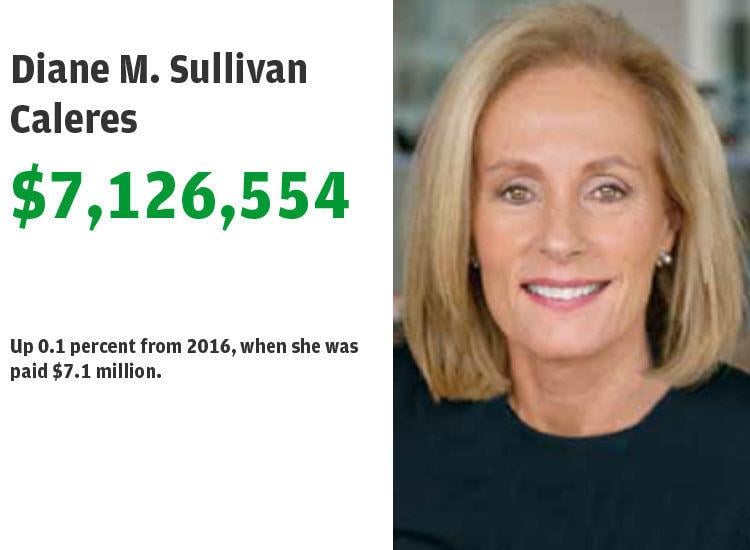

12. Diane M. Sullivan, Caleres Inc.

. Median pay for its 12,055 workers was $21,528 (about 40 percent of its employees are part-time/temporary/seasonal).

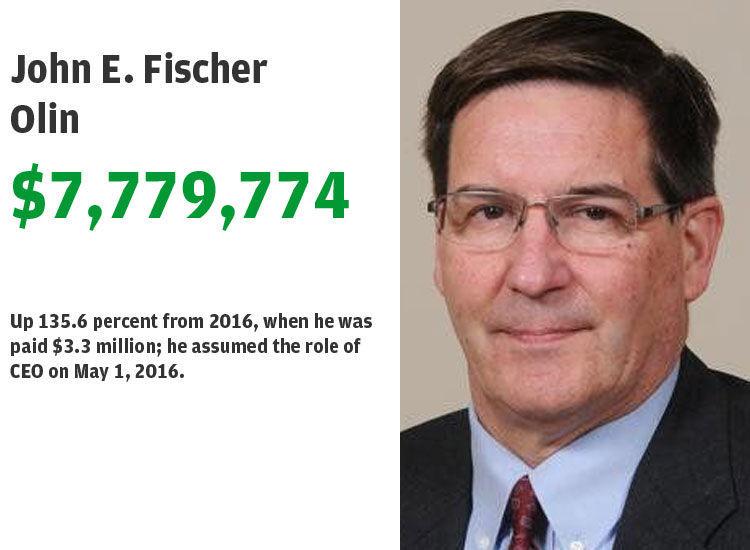

11. John E. Fischer, Olin

. Olin employs 6,526 people worldwide.

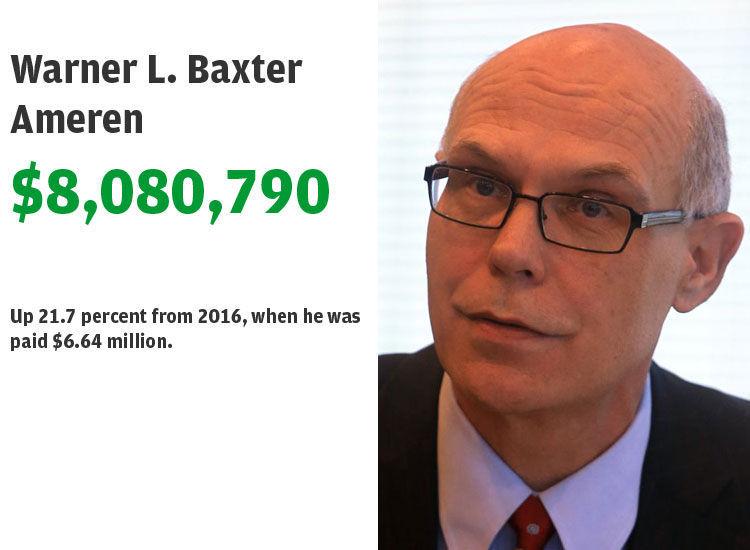

10. Warner L. Baxter, Ameren

;╠²Baxter earned 66 times as much as the median Ameren employee. Ameren employs 8,600 people and says they earn a median of $122,003.

9. Robert V. Vitale, Post Holdings

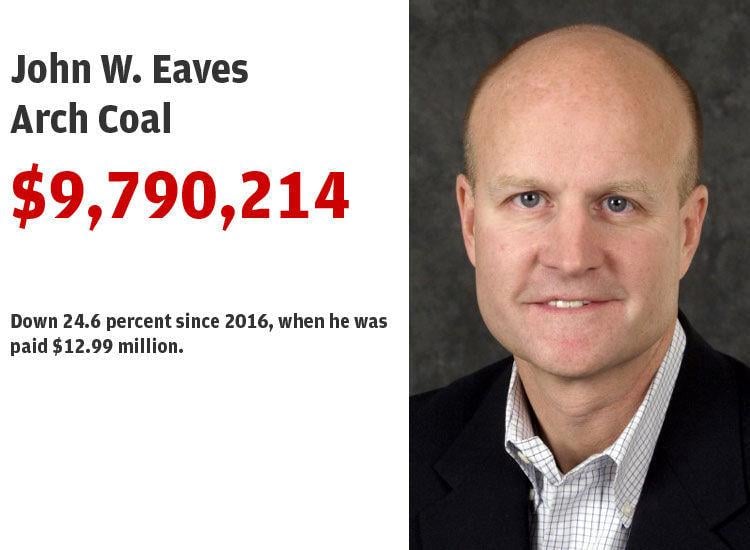

8. John W. Eaves, Arch Coal

.

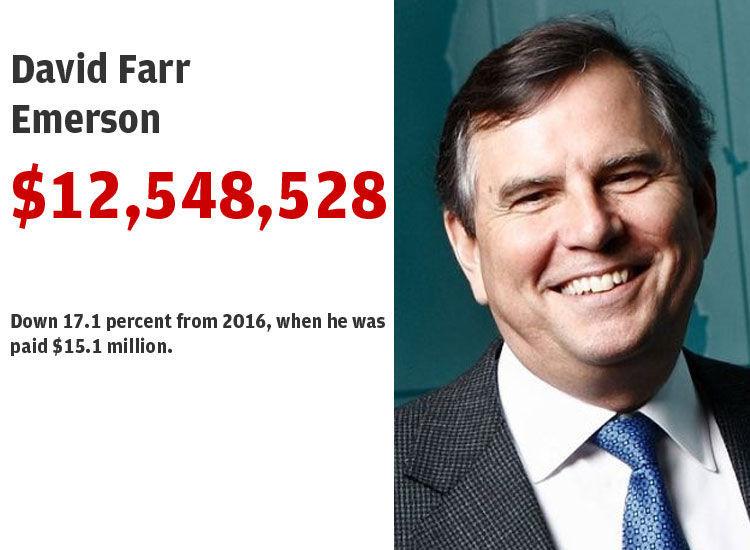

7. David Farr, Emerson

From February:

6. Ronald J. Kruszewski, Stifel

Stifel reported that its CEO earned 92 times as much as its median employee. .

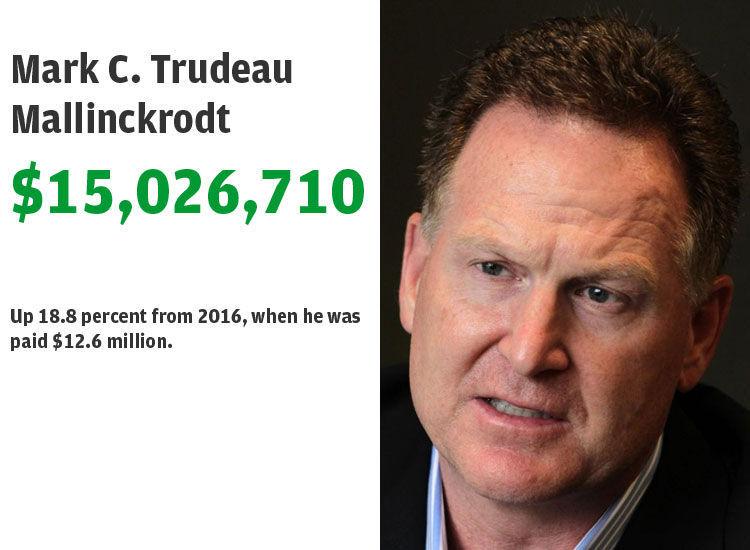

Mark C. Trudeau, Mallinckrodt

; Mallinckrodt CEO Mark┬ĀTrudeau's pay in 2017 was 102 times as much as the median company employee, who earned $146,870.

4. Timothy Wentworth, Express Scripts

. Median pay for its 26,600 workers was $52,509.

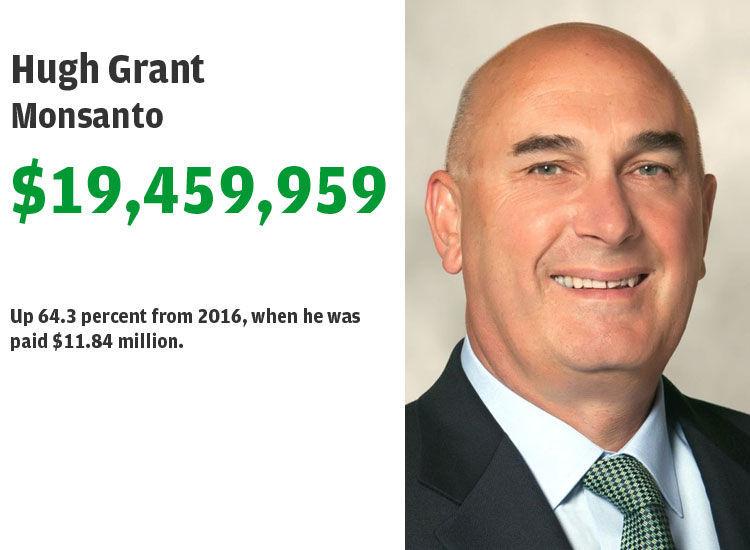

3. Hugh Grant, Monsanto

From April:

2. Glenn L. Kellow, Peabody Energy

. Peabody's 7,148 employees in the United States and Australia earned a median $118,812 last year.

1. Centene, Michael Neidorff

The CEO earned 379 times as much as the median Centene employee, . The company's 33,312 workers earned a median $66,600, including medical premiums.

.╠²